Getting Started With Savings

- 30 May 2024 2:25 PM

The earlier you begin trying to save, the easier you’ll make things for your future self.

When you’re in your 20s, retirement seems so abstract, it might as well be thousands of years away.

Maybe it feels something like that to you right now. Why save for something so many decades in the future, when every last dollar is accounted for in the here and now? Saving for anything at all, in fact, may feel impossible.

But what if you just laid the groundwork so that it became easier to save a little something? That’s what we’re going to work on today.

Getting started early for retirement is smart for the same reasons you may want to put it off: Time is on your side. If you set aside what you can now, the magic of compounding numbers — when you begin to earn interest on interest — can do more of the heavy lifting over time.

In other words, saving early may result in having to save less over the long haul, which will take some pressure off as you’re juggling other demands that inevitably arise. Maybe those demands will be children and all the money they manage to siphon up, or perhaps you’ll need some time off to care for an aging parent.

And (mostly) nobody wants to work forever — the earlier you start saving, the sooner you can stop working and dedicate more time to what’s meaningful to you.

The easiest way to save — for everything, really — is automating. When you have money automatically and regularly shuttled to its destination, you don’t have to remember to do anything. That goes for purely pleasurable financial goals as well, like saving for a big trip.

It’s empowering, and will bring you closer to the things that make you both happier and more financially secure. It will take some time and patience — but your future self will thank you.

Before you get started, you need to figure out how much you have to work with.

- Deal with debt. Before you begin saving, make sure you have a plan to knock out any high-cost debt, like debt on credit cards, where interest rates (around 22 percent) far exceed the money you might earn when investing your savings in the stock market over time (7 to 8 percent).

- Get organized. Get a copy of your pay stub or check your direct deposit to get a sense of your take-home pay. (Freelancers should calculate their average monthly income.) Then write down all of your expenses — rent, all insurance not already deducted from your paycheck, utilities, groceries, transportation costs, car payments, mobile phone, student loans and any other debts.

How much is left over? Something? Congratulations! You have some room to save. Cutting it close? Is there anything you can pare back a bit to make space for some savings? - Build a Buffer. Creating a financial cushion — in the form of an emergency savings fund — can help you avoid turning to credit cards if you suddenly lose your job or hit a financial pothole, like covering a $1,000 car repair.

Financial planners suggest keeping three to six months of your expenses in emergency savings (stowed in a high-yield online savings account, which offer the best rates). That may seem like a lofty goal when you’re living on a starting salary that barely covers your bills. So start small, even if it’s saving $50 a month — $83 a month will get you to $1,000 in a year — and add more if and when you can afford it. Set up an automated plan that sweeps that amount from your checking account to your savings account. Then, don’t touch that money.

Saving for Retirement

Many people with student loan debt often wonder if they should focus on paying down those loans before saving for retirement. The short answer: Probably not. (If you’re really struggling to pay your federal student loans, check out the income-driven repayment plans I mentioned yesterday.)

But there’s a strong case to be made to both invest and pay down your loans simultaneously, if you can.

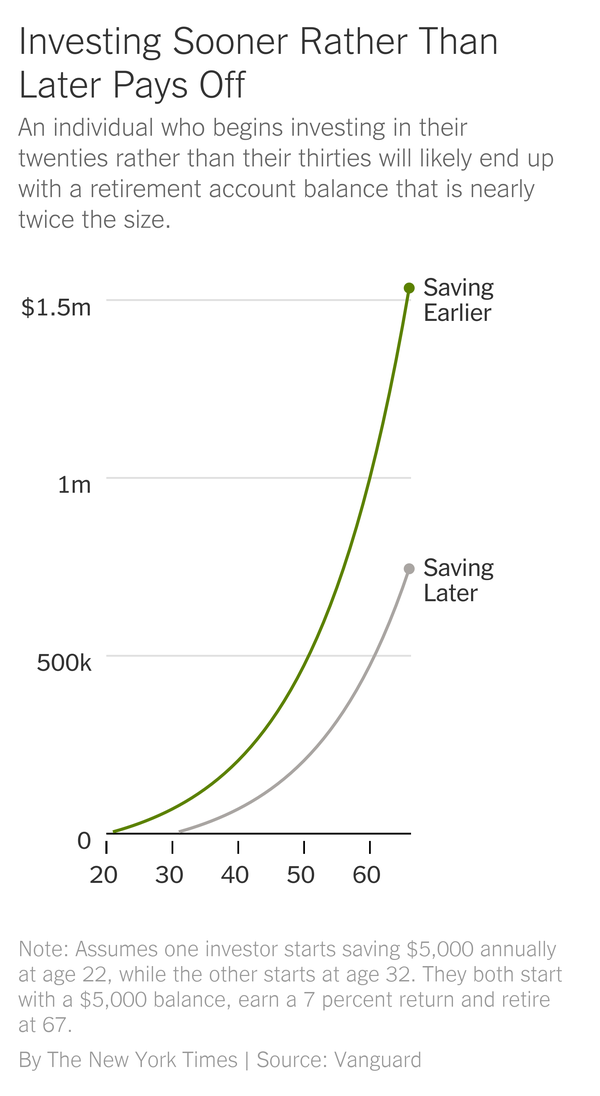

The illustration below practically screams why. Can you see how much you’re likely to give up by focusing solely on paying off loans for 10 years?

Image

If you have access to a 401(k) or a similar workplace retirement savings plan, you’re in luck — only 69 percent of private-sector workers do.

You may have already heard that some plans come with a nice little perk: free money. Employers may provide matching contributions when you save; for example, they might match every dollar you contribute up to 4 percent of your salary.

That means you’re effectively contributing 8 percent of your income, which is pretty close to the 10 percent that experts recommend (they often recommend saving more, up to 20 percent, but 10 percent is a great start — consider ratcheting it up one percentage point each year as you get raises).

What if you don’t have a workplace retirement savings plan?

Roth individual retirement accounts (or Roth I.R.A.s) are often the right choice for younger people (though they are subject to income and contribution limits). That’s because you’re depositing money that has already been taxed, and you’re probably in a lower tax bracket now than you will be later in life, when you’re likely to be earning more.

Compare that with the traditional I.R.A., which provides you with a tax deduction now, but you pay income taxes when the money is withdrawn. That means your Roth I.R.A. balance is what you’ll have to spend, whereas traditional I.R.A. balances will be reduced by the amount of tax you will owe later.

How should you invest your money? The short answer: A diversified mix of index funds. These are inexpensive mutual funds that track broad spheres of the stock and bond markets (exchange-traded funds, which are like mutual funds but trade in an exchange, are a similar option). For more details on your investment options, check out this guide.

More immediate spending goals

Besides retirement, you surely have other savings goals. Maybe you’re saving for a car, a wedding party or a special trip. Since these goals have a shorter time horizon than retirement, or something you’ll need to access within three years or less, you’ll want to take less risk with this money. The easiest strategy is to automatically transfer money into a high-yield online savings account, say, monthly. With short-term goals, the amount you save is far more important than your return.

But if you need the money in three to 10 years — call that a medium-term goal — you may have more options, depending on how flexible you can be with your timing.

It may be tempting to invest your savings in the stock market, for example, in hopes of generating a higher investment return. But that comes with more risk. As one financial planner wisely put it: You have to consider how it might feel to lose half of your stock investment in any given year, which can take some time, even years, to recover. Do you have the time (or the stomach) for that?

You can take a hybrid approach and invest in a mutual fund that has a mix of 60 percent bonds and 40 percent stocks, for example, or there may be bond investments to explore that provide more stability (though they carry risks of their own). But tread carefully.

Even if you don’t have large amounts to save now, setting up the infrastructure to save is the hardest part — and as your earnings increase, it will be much easier to save and invest more.

Action items:

- Do you have a high-yield online savings account? Some banks, including Ally and Capital One, let you set up different savings buckets for specific goals, which you can label (emergency funds, vacation, down payment). DepositAccounts.com has a helpful guide to help you sort through options.

- If you have a workplace retirement plan and haven’t thoroughly inspected the investment options, set a reminder in your phone’s calendar to check. What index fund options do they have on offer? Also familiarize yourself with any target-date fund offerings. (These are a ready-made mix of investments that you can select and then forget about and are a blend of stock and bond mutual funds that gradually and automatically become more conservative as you approach the year you expect to retire. If you were born in 2000, the 2065 or 2070 funds may be the right fit for your situation.)

- If you don’t have access to a workplace retirement plan, familiarize yourself with roboadvisers, or companies that lean heavily on technology to manage your investments but also often have human financial advisers. These are nice options for people with simple needs, or who have a savings and investment plan they want to establish and run on autopilot. Morningstar ranked its top picks here.